I’m fascinated by the tools, banks, and major elements that create each person’s solution to handling their money. Inspired by Peter Kang and Matt Lebel’s take on how they organize and allocate their finances, I want to share my approach to how I tackle the challenge. This is a snapshot of my financial life in 2019:

Background

22 years old / new grad (BCom) / Montreal, Canada (coming from Vancouver)

Source of Income

I’m currently employed full-time in a marketing position for a CPG company. Before I graduated university in April, I was working as a TA on contract, making some extra money alongside my studies (~$1,000). My gross income (if I worked all of 2019) is within the $50,000-$70,000 range.

Main Expenses

Housing - I’m currently living in a 1 1/2 studio in downtown Montreal and pay $950 a month for rent, internet, and utilities. Work and groceries are only around 10 mins away so I don’t need public transportation during my day-to-day life.

Food - I meal prep for 3 or 4 days out of the week, with the rest being meals where I dine out. My food split is currently 50/50 between groceries and dining (about $600 total). I purchase on average two cups of coffee these days from work (~$1.25/cup).

Phone - I’m in a 10GB data family plan with my parents and sister, and my portion of the bill is $55.

Student Loans - My student loan grace period just ended and now I’m liable to pay my part to the feds ($6-$8K). My parents were kind enough to give me a lump sum to pay for all of my debt upfront so that I could avoid additional interest, so I plan on paying them back over a 2 to 3 year period (around $250/month).

.Other - Additional expenses that occur often would be subscriptions where I pay around $30/month - Spotify, Amazon Prime, Squarespace, etc.

Banking

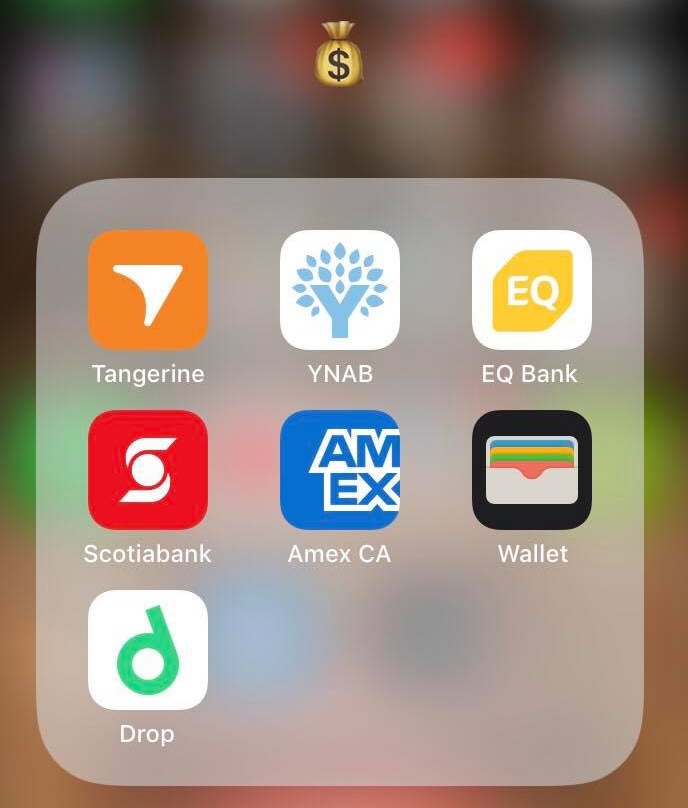

Tangerine (Daily Banking) - If you know me, what did you expect? I used to work for them! Tangerine is straightfoward free banking, meaning no monthly fees, unlimited transactions, no minimum balances… forever. The only drawback that’s highkey visible is the lack of free e-transfers (it’s $1 each), but I can live with that. I keep my daily chequing and savings account with them, along with my direct deposits. The chequing is used to make debit transactions (there aren’t that many) and bills, while my main savings account is a reserve that I use to hold monthly rent and credit card payments.

What’s also cool about Tangerine is their Recipes - meaningful and creative ways for you to move, manage and save your money. Check out some of them below! I currently use two of them: Top Up (for my chequing account), and Round Up (to the nearest $2 - the excess savings get invested).

Interest Rate (Chequing): 0.15% | Interest Rate (Savings): 1.15%

EQ Bank (Emergency Fund + Short-Term Goals): The best wordto describe EQ Bank is “amazing”. One of the highest savings account interest rates in Canada, unlimited e-transfers, ability to pay bills… it does it all. I keep my emergency fund here along with my vacation savings. If I ever decide to save up for a down payment on a house (LOL), this is also where the money will be.

Interest Rate: 2.30% (!)

Credit Cards

American Express Cobalt - My main credit card, and the only one I have that has a monthly fee ($10). It’s a membership rewards card with an approximate 5% (5 points/dollar) rewards rate on all food purchases (groceries + restos), 2% on travel and transportation, and 1% on everything else. Points can be redeemed for flights, Ticketmaster purchases, Amazon, and hotel programs! This card felt like a great fit for me given my spending habits and goals, and I signed up with a promo link that gives me a complementary $100 Ticketmaster voucher which almost pays back the first year’s monthly fees.

Tangerine Cash Back Credit Card - My secondary credit card for when the store doesn’t accept AMEX- 2% cash back for three purchase categories, and 0.5% for the rest. My 2% categories are groceries, restaurants, and drugs stories and I usually get anywhere between $10-20 back a month (most cash-back credit cards pay your cash back annually, this one doesn’t!)

Scotiabank SCENE Visa - The first credit card I got. Effectively a 1% rewards rate card that I can use toward Cineplex movie tickets and various restaurant partners (Milestones, Biergarten, etc.). It pays for dates with the GF!

Drop (App) - Additionally, I use an app called Drop. It’s a loyalty rewards program that links to my existing credit cards and I earn points when I shop at places like McDonald’s and Shoppers Drug Mart, which I can then redeem for prizes (think gift cards from Amazon, Foodora, Indigo, etc.). I’ve written more about Drop here.

Investing

Wealthsimple - Investing made easy via a robo-advisor that automatically puts my money into index and bond ETFs (at a risky 90/10 allocation since I’m young). I keep my long-term money in there. I save 25% of my paycheque and deposit it automatically to my account.

While I could cut down the investing costs through DIY and purchasing ETFs myself, I’m lazy and know I would start trying to actively play around with my money. Wealthsimple takes that away from me. I also don’t have the mobile app because I know I’d be checking it excessively for updates throughout the day!

Their marketing team is also on fire.

Management Fee: 0.7% of investments ($7 per $1,000 invested)

Budgeting / Net Worth Tracker

You Need A Budget - I keep a monthly budget and record my daily transactions with YNAB ($7 USD/month). What I like about it is that it’s a proactive way to manage my money - I have to proactively input my transactions, look at the money I spent every few days, and routinely see how I’m doing vs. my original budget rather than looking back on money that’s long gone a month ago.

YNAB relates to a money philosphy that I genuinely believe - You have to be intentional about money you use up, and you need to get comfortable looking at your money for real change in your spending habits to happen.

Knowledge and Education

r/PersonalFinanceCanada - My #1 resource for what’s happening in Canada pertaining to personal finance. Real stories, questions, and answers from real Canadians.

The Globe and Mail - The Investing: Personal Finance section is a great place for editorial articles and what I would consider “national” personal finance knowledge and issues. Unlike most of the Globe’s frontpage articles, the personal finance section is mostly free and Rob Carrick is a gem!

Podcasts - I enjoy listening to Mo’ Money by Jessica Moorhouse as well as Canadian Couch Potato by Dan Bortolotti. Occasionally, I listen to Optimal Finance Daily during my walk to work.

Money Outlook

The goals ahead - Tentative. The big savings goal that I have in mind right now would be to put money aside for a great trip abroad in 2020.

During the summer, my main priority was saving up for an emergency fund that can cover three to four generous months of expenses ($7,000) in case shit hits the fan. Additionally, since I had to move out of my sublet at the end of August, I saved up $1,500 for moving and furnishing costs in September.

The down payment on a house can wait…

Pay yourself first - When the direct deposit hits, I take out 25% of my money right away to “pay” my Wealthsimple investment account. 25% emergency.. I don’t touch it after. I also transfer half of my monthly rent + utilities into my savings ASAP. It’s my loose adaption of the 50/30/20 budgeting rule.

You only live once - I’m young, so I might as well live it up and spend spontaneously sometimes. You’re only 20/21/22/23/whatever for so long… you know?

Stay curious about money - From a Peter Kang quote on his own personal finance stack post - “The most important thing is to stay curious, continue absorbing new information, and to admit that I know very little.”